Posts in category 'The Savvy Realtor'

Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

- 2022 | 15 Posts

- 2021 | 24 Posts

- 2020 | 26 Posts

- 2019 | 11 Posts

- 2018 | 6 Posts

- 2017 | 3 Posts

- 2016 | 19 Posts

- 2015 | 4 Posts

20

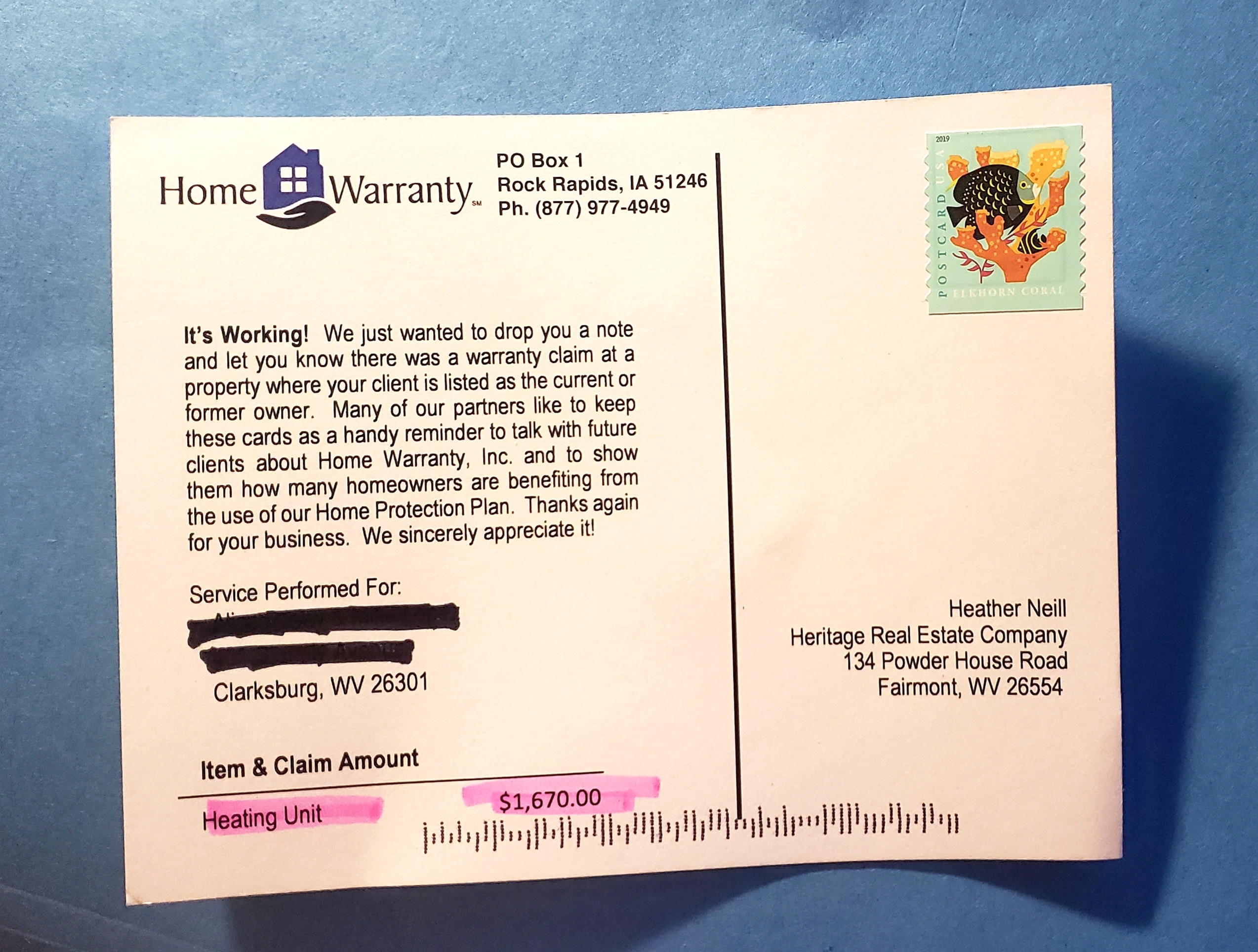

Home Warranties - Do I Need One?

We always get a little postcard when Home Warranty Inc. covers a claim for one of our buyers or sellers; it makes us feel good to know our folks are protected in the event of some unforeseen problem with their new home.

Home Warranty Inc. gives great service (we love their 14-month warranties!) and, in the six years we've been using them, we have never had them turn down any legitimate claim. In an area such as north-central West Virginia, where our housing inventory is comprised largely of older homes, nothing could be more important than feeling secure in your home!

Like any insurance policy, home warranties come in many shapes and sizes, with various coverages and caveats. Does every home need a home warranty? Probably not. But we can guide you through this protection option as part of our complete package of services for o...

28

Mortgages - Six Things You Need to Know to Save Big Money

Most of us make our house payment every month without ever thinking about how we are really spending our money. The fact is, if you purchase a $200,000 house January 1, with zero down, at 5% interest, on a 30-year fixed note, you'll be making a monthly principal and interest payment (not counting PMI, property taxes, and homeowners' insurance) of about $1,073. Some $833 of that monthly payment will go toward interest, and only about $240 to your principle balance. The first year alone will cost you almost $10,000 in interest. Over the life of the loan, you will pay some $186,511 in interest – almost double the cost of the home.

THE TAX DEDUCTION MYTH

What they say: "But...

22

Should I Rent My House While I Try to Sell It?

Home sellers sometimes ask me whether renting their house while we're trying to sell it is a good idea. Particularly if they have moved on to a new job and home, and are now carrying two mortgages, they can be in very real financial trouble. Sometimes divorce is the culprit, as spouses and homes are torn apart, incomes separated, with two sets of living expenses where once there was one.  I have seen sellers have their homes repossessed in circumstances such as these, when a renter may very well have prevented foreclosure.

I have seen sellers have their homes repossessed in circumstances such as these, when a renter may very well have prevented foreclosure.

Renting your house while you try to sell it can be a great option financially, assuming the renters pay the rent on time and don't tear the place up, leaving the homeowner to have to facilitate repairs in order to sell the home. Some renters are wonderful, caring for a home like it were their own. They mow the yard, paint th...

27

Closing Costs: What's that Set of House Keys Going to Cost Me?

"Closing costs" is a confusing term. Depending upon who you're talking to, it can encompass various monies which will be required of a buyer in order to get up from a closing table with a new set of keys (hopefully with a  Heritage Real Estate keyring attached). There are numerous charges and fees involved and buyers frequently get the terms mixed up. More often than not, neither lenders nor Realtors thoroughly and clearly explain things to the buyer.

Heritage Real Estate keyring attached). There are numerous charges and fees involved and buyers frequently get the terms mixed up. More often than not, neither lenders nor Realtors thoroughly and clearly explain things to the buyer.

Firstly, there is a difference between "closing costs" and "down payment," something first-time buyers frequently misunderstand. I recently had a deal go south because the buyer's agent didn't bother to explain to him that "zero down" didn't mean there were no costs involved. Imagine his surprise when, two weeks into our contract, he learned he had to come up with $4,000 in closing costs.

Your "down paymen...

17

The Danger in Doing the Deed - Pitfalls for Unmarried Home Buyers

I was sitting in a local coffee shop with a nice, young couple giving them my crash course in first-time home buying; everything from loan pre-approval to the costs involved, to inspection contingencies and contract clauses.

They'd dated since high school, been engaged for a couple of years, were about to be married, and ready to start shopping for their first home. "Is there anything we need to know," he asked, "since we're not married yet?" It was an astute question.

A lot of things have changed about the real estate business since I got into it nearly 20 years ago, including the number of unmarried young people buying homes together. A surprisingly common scenario is one in which young, first-time home buyers have only been dating a few months and decide to save on rent and buy a house. Often, one of...

207 Aurora Dr

Morgantown, WV 26508

WEST VIRGINIA LICENSES BROKER WVB240300963

AGENCY 010271-00

Translate

Translate

Office License No. 010271-00